Does Homeowners Insurance Cover Mold? What You Need to Know

Usually no. Most homeowners insurance policies exclude mold unless it resulted from a sudden covered water event like a burst pipe. Even when covered, policies typically cap mold remediation at $5,000 to $10,000. Professional mold removal costs $3,000 to $30,000. Document everything from the moment of the water event if you want any chance of coverage.

When insurance covers mold (and when it does not)

Covered: Mold that results directly from a sudden, accidental water event that is itself a covered peril. A burst washing machine hose that soaks the wall and grows mold: covered. A water heater that fails and floods the basement: covered. An accidental fire sprinkler discharge: covered. The key words are "sudden" and "accidental."

Not covered: Mold from gradual problems. A slow roof leak you did not repair. Condensation from poor ventilation. High humidity from a missing vapor barrier. A dripping pipe you noticed months ago but did not fix. Flooding (which requires separate flood insurance through FEMA's National Flood Insurance Program). Foundation seepage. Poor maintenance of any kind.

Insurance companies view mold from gradual problems as a maintenance issue, not an insurable event. Their position is that homeowners are responsible for maintaining their home and addressing moisture problems before mold develops. Whether you agree with that or not, it is how most policies are written.

The gray area: A hidden pipe leak inside a wall that you did not know about. You did not neglect it because you had no way to know it existed. Many claims in this category are initially denied and then approved after appeal or adjuster negotiation. Documentation is critical for these cases.

Mold caps: the hidden limit in your policy

Even when your insurer agrees to cover mold, there is almost always a cap. Most standard homeowners policies limit mold coverage to $5,000 to $10,000. Some policies cap it as low as $1,000. This cap applies regardless of how much the remediation actually costs.

Professional mold remediation costs vary widely based on the extent of the problem. A small area (under 10 square feet) in one room runs $500 to $3,000. Multiple rooms with wall cavity involvement runs $5,000 to $15,000. Whole house contamination with HVAC involvement can reach $15,000 to $30,000 or more.

If your remediation costs $20,000 and your policy cap is $10,000, you pay the remaining $10,000 out of pocket. This is why prevention is so much cheaper than remediation. A dehumidifier costs $200 to $400. A vapor barrier costs $1,500 to $3,000. Fixing a leaking pipe costs $150 to $500. All of these prevent problems that cost $10,000 or more to remediate.

Mold endorsements: Some insurers offer optional mold coverage endorsements (riders) that increase the cap to $25,000, $50,000, or even $100,000 for an additional premium. If you live in a humid climate, have a basement or crawl space, or have had past water damage, this endorsement is worth considering. Call your insurer and ask specifically about mold coverage limits and available endorsements.

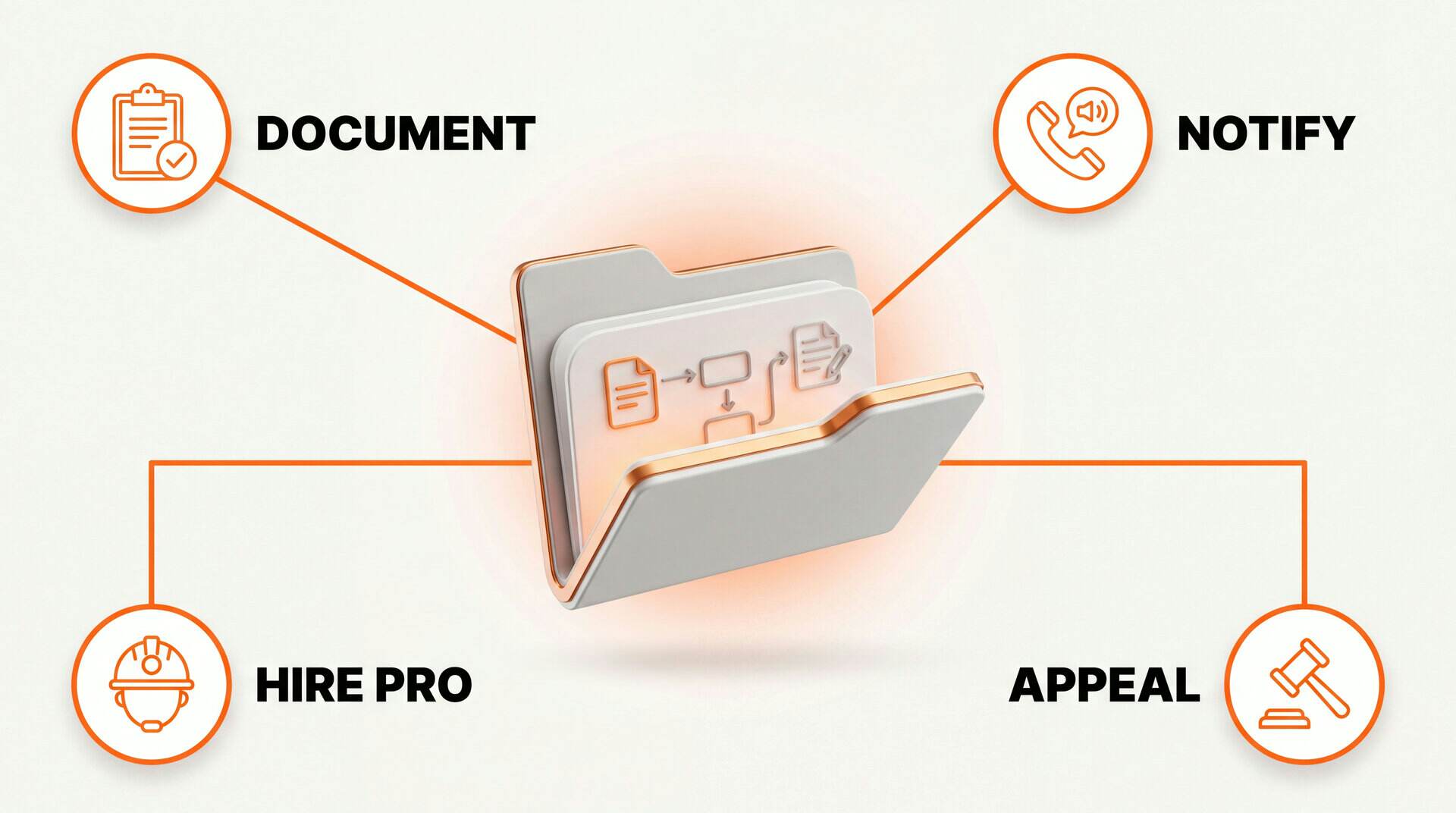

How to document a mold claim

If you discover water damage that could lead to mold, start documenting immediately. The quality of your documentation can make or break a claim.

Step 1: Document the water event. Take timestamped photos and video of the water damage as soon as you find it. Show the source (burst pipe, failed appliance, etc.) and the extent of the damage. If you called a plumber or water mitigation company, save every receipt and written report.

Step 2: Mitigate immediately. Your policy requires you to take reasonable steps to prevent further damage. This means stopping the water source, removing standing water, and starting the drying process. Failure to mitigate promptly can be used to deny the mold portion of the claim. Document your mitigation efforts with photos and receipts.

Step 3: Hire an independent mold inspector. Get a written inspection report from a licensed mold inspector who is not affiliated with any remediation company. This removes conflict of interest. The report should document the type and extent of mold, the moisture source, and recommended remediation. This is your evidence that the mold is a direct result of the covered water event.

Step 4: Get multiple remediation estimates. Get written estimates from at least two IICRC certified mold remediation companies. The estimates should detail the scope of work, timeline, and cost. Having multiple estimates shows the insurer that the costs are reasonable and industry standard.

Step 5: File the claim promptly. Most policies require timely reporting. Waiting weeks or months to file a mold claim gives the insurer reason to argue you did not mitigate promptly or that the mold is from a separate, uncovered source.

Step 6: Keep a communication log. Write down every phone call with your insurer: date, time, person you spoke with, and what was said. Follow up every phone call with a written email summary. If the claim is denied or reduced, this log is your evidence for an appeal.

What to do if your claim is denied

Read the denial letter carefully. It must cite the specific policy language used to deny the claim. If the reason does not match the facts, you have grounds for appeal.

Appeal in writing. Send a formal written appeal with your documentation: photos, inspection reports, remediation estimates, and a clear argument for why the mold resulted from a covered event. Reference the specific policy language they cited and explain why it does not apply.

Hire a public adjuster. A public adjuster works for you, not the insurance company. They review your policy, inspect the damage, and negotiate with the insurer on your behalf. They typically charge 10 to 15% of the claim payout. For large claims, this investment often results in significantly higher payouts.

Contact your state insurance commissioner. If you believe the denial is unfair, file a complaint with your state's department of insurance. The insurer must respond to the complaint, and the state may mediate on your behalf.

Consider an attorney. For claims above $10,000 that are wrongly denied, an insurance coverage attorney can be worth the cost. Many work on contingency (no fee unless you win). Bad faith denial of a legitimate claim can result in damages beyond the policy limits.

Document your mold problem before calling insurance

Our app walks you through 160 professional mold hotspots room by room. Same checklist professional mold inspectors use. AI powered photos and verdict in 30 seconds. Use it as documentation for your claim.

Get Early AccessFrequently Asked Questions

Does homeowners insurance cover mold removal?

Usually no. Most standard homeowners insurance policies exclude mold damage unless the mold resulted directly from a sudden, covered water event like a burst pipe or appliance overflow. Long term moisture problems like slow leaks, humidity, condensation, and flooding (which requires separate flood insurance) are typically excluded. Even when covered, most policies cap mold remediation at 5,000 to 10,000 dollars.

When does insurance cover mold?

Insurance covers mold when it is the direct result of a covered peril. Examples: a washing machine supply hose bursts and soaks the wall, a water heater fails and floods the basement, or a fire sprinkler accidentally discharges. The key is that the water event must be sudden and accidental, not gradual. If you knew about a slow leak for months and did not fix it, the resulting mold is not covered because failure to maintain the home is excluded.

What is a mold cap on insurance?

A mold cap is a maximum dollar amount your insurance policy will pay for mold remediation, even when the mold is from a covered event. Most policies cap mold coverage at 5,000 to 10,000 dollars. Professional mold remediation can cost 3,000 to 30,000 dollars depending on the extent. If your remediation costs 20,000 dollars and your cap is 10,000, you pay the other 10,000 out of pocket. Some insurers offer mold endorsements that increase the cap for an additional premium.

How do I document mold for an insurance claim?

Document everything from the moment you discover the water event. Take photos and video of the water damage and any visible mold with timestamps. Save all repair receipts. Get a written report from a licensed mold inspector (independent from the remediation company). Get written remediation estimates from at least two companies that follow the IICRC S520 standard (ACAC, RIA, or state-licensed also qualifies). File the claim as soon as possible because delays can be used to deny coverage. Keep a written log of all communication with your insurer.